Global Consumer Packaging, UK Division

An underperforming division needed forensic cost analysis to determine source of profitability problems.

CHALLENGE

Identify causes for lack of profitability in an injected mold and blow molded packaging producer and recommend remedies. Producer had #1 market share position in the UK due to exclusive supply agreement with P&G, but was severely underperforming goals, actually making a loss.

Cost driver analysis revealed the deep profitability problem of the highest volume products and the deep profit pool of the low volume items.

SOLUTION

Structure an analysis to determine true drivers of cost in the manufacturing operations, and then recast the costs across the product portfolio to determine true profitability of products and sources of profitability or lack thereof. Analysis determined that the P&G product items were the least profitable in the portfolio and that low volume, specialty packaging products—which had been targeted for de-emphasis—were the most profitable and generated the most free cash. It was also determined that excessive handling of the product was being driven by standard cost rules which dictated internal performance measures based on machine rates for efficient production. To keep individual machines at maximum run rates, and so capture maximum accounting payout rates, the machines were kept disaggregated, necessitating WIP inventory and boxing and unloading of parts between operations.

ACTIONS TO IMPROVE PROFITABILITY:

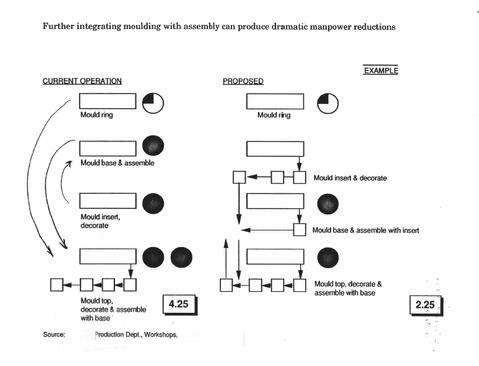

Joined blow molding machines to decorating machines in a cell fashion to eliminate excessive handling between machines.

Redirected sales team to find more small volume specialized container business despite higher set-up costs due to prices which were 2x to 5x the prices of commodity products.

Used the forensic cost analysis to successfully renegotiate pricing with P&G by showing that current contract costing could barely cover resin costs.

Spaghetti (tracing product through the plant) & standard work cycle time analysis revealed opportunity to reduce double handling.

BENEFITS

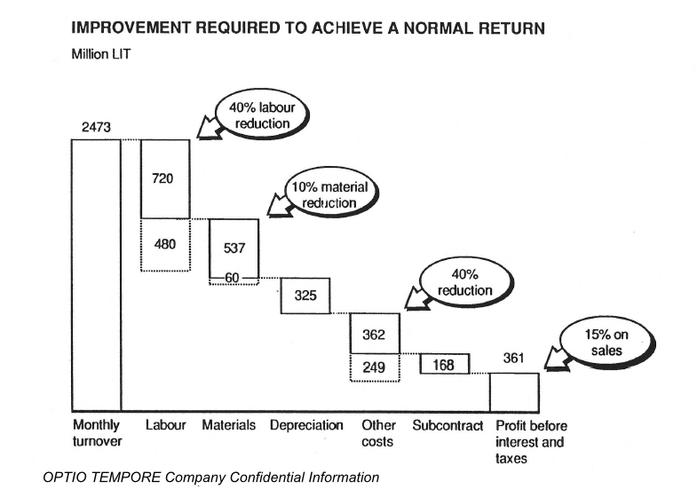

We saw a 40% reduction in hourly workforce, a 40% margin increase, and a 10% reduction in material costs.

The combination of operational cost reductions and price improvements returned the division to profitability in line with the rest of the company.